SELF EMPLOYED BORROWERS

Changing with the Times

SELF-EMPLOYED BORROWERS

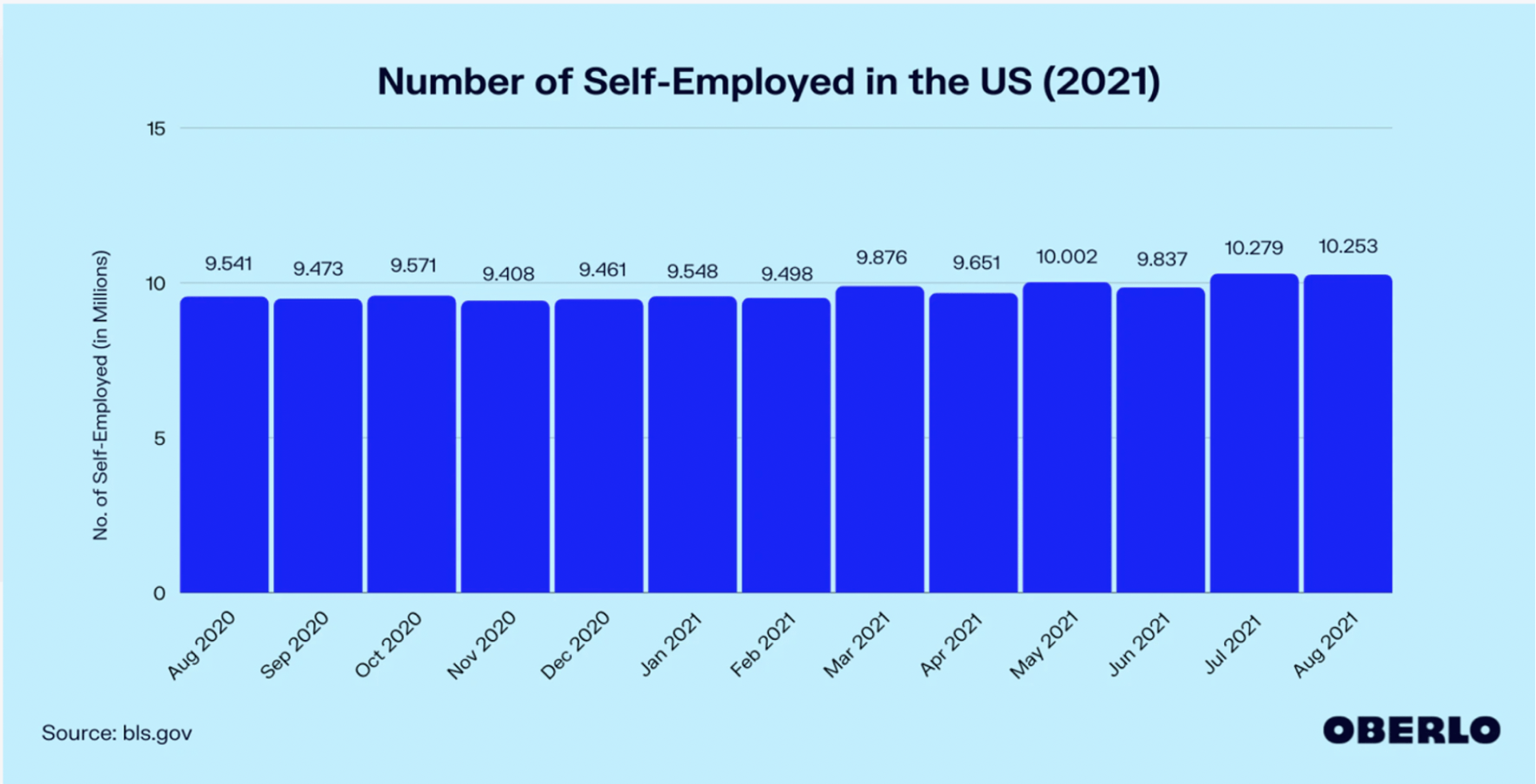

The meaning of an “average borrower” has change throughout the years. Today, many borrowers are self-employed, work remotely and have a different family composition than in the past. The U.S. Bureau of Labor Statistics shared in August 2021, that there are over 10 million self-employed people in the US. That is almost a one million increase from the year before.

Included in the self-employed workers, are independent contractors and freelancers who may work for multiple clients, do short-term assignments or have multiple streams of income coming in. This current demographic of self-employed is expected to rise. (see the chart above from bls.gov and Oberlo)

Verifying Self-Employed Income

How do lenders verify the self-employed borrower’s income when applying for a loan? The lender may verify a self-employed borrowers’ employment and income by obtaining from the borrower copies of his or her signed federal income tax returns (both individual returns and in some cases, business returns) that were filed with the IRS for the past two years (with all applicable schedules attached).

Alternatively, the lender may use IRS-issued transcripts of the borrower’s individual and business federal income tax returns that were filed with the IRS for the most recent two years – as long as the information provided is complete and legible and the transcripts include the information from all of the applicable schedules.

When two years of signed individual federal tax returns are provided, the lender may waive the requirement for business tax returns if:

- the borrower is using his or her own personal funds to pay the down payment and closing costs and satisfy applicable reserve requirements,

- the borrower has been self-employed in the same business for at least five years, and

- the borrower’s individual tax returns show an increase in self-employment income over the past two years.

For certain loan casefiles, lenders may permit only one year of personal and business tax returns, provided lenders document the income by:

- obtaining signed individual and business federal income tax returns for the most recent year,

- confirming the tax returns reflect at least 12 months of self-employment income, and

- completing a cash flow analysis form that applies the same principles.

Times Have Changed

Another factor to take into consideration, besides the various ways borrowers are now generating their income, is the change in the family composition of the borrowers. Today, household income can come from multi-generational families all living in the same home. That means the family’s income can come from an economic support system composed of non-traditional relationships, instead of spouses, who would typically apply for a mortgage together.

The latest changes in employment trends and family financial dynamics, creates a need for mortgage products to meet these growing variations while, still considering the borrower’s ability to repay. One of the struggles mortgage brokers face with this new trend, is finding lenders that offer solutions outside the traditional, conventional mortgage box. These situations require more creativity and innovation, from lenders who are willing to work with borrowers.

Something else to be considered, is income or employment disruptions to the borrower during the pandemic. It is important to find the right lender that can take a look at the specific situation and its relationship to the times we live in.

Once the right lender is found, the broker keeps clear and consistent communication with the lender’s underwriting department, assuring that the borrower can get to the closing table quickly and efficiently. Communication is a key element with the unconventional lending situation, where more documentation may be required or, borrowers may have to jump through more hoops to show their income, employment history or verify their self-employed business earnings.

As a mortgage broker, I work with lenders offering non-QM loan programs that provide self-employed borrowers with more options and creating tailor made products.

Whatever kind of borrower you are, lenders are providing a suite of products to help even the most unique borrower afford a home. Contact me today to learn what programs might be in place to help you purchase or refinance a home.

Jim Stojak

President/CEO NMLS# 242917

Palm Harbor Mortgage Advisors, Inc NMLS 1948608

727-542-3357